This study looks at TV advertising's often-hidden contribution to response in the short, medium and long-term.

In Brief

The world of response planning has become increasingly complex over recent years. Understanding the key drivers of response over the short, medium and long-term is a constant challenge, but one that’s essential if advertisers are to optimise their investment.

GroupM were commissioned to analyse the response effects of a wide range of channels. These included both brand and direct response TV, radio, print, outdoor, direct mail, affiliates, online display and paid online search. Through a unique combination of analytics methodologies, including econometric modelling and GroupM’s Spotlift tool the effects of communications were measured over the immediate, short to medium-term and long-term.

Key findings

- TV creates the highest volume of short to medium-term sales. It drives more media-driven sales than any other communication channel.

- TV advertising drives the highest volume of cost-efficient response: because of its reach and scale, TV advertising keeps generating a cost-efficient level of response at higher levels of spend than other media.

- TV advertising dominates longer-term response. Half of all media driven response comes 3-24 months post campaign and TV is responsible for 52% of the impact that media has in the longer-term.

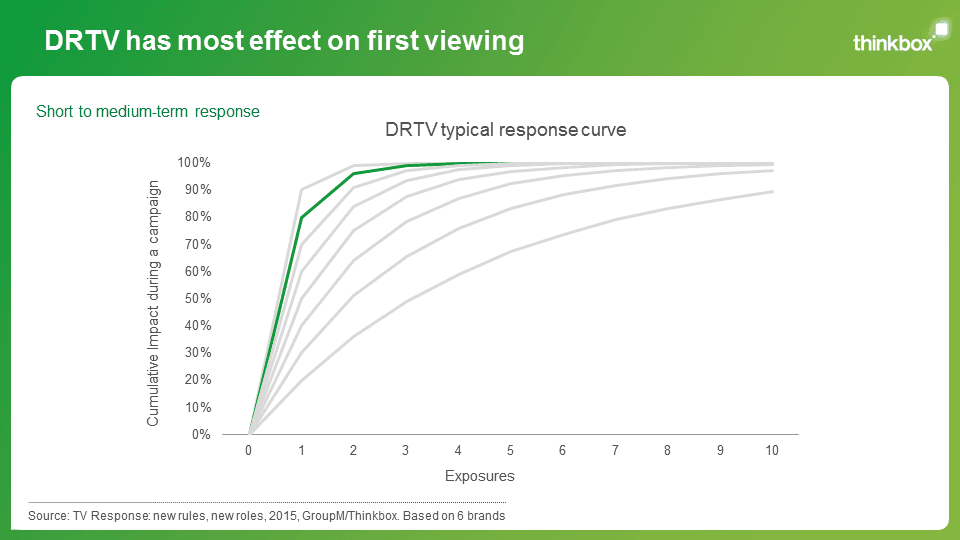

- Direct response TV should be planned to maximise coverage above frequency – c.90% of total response was generated after a viewer had seen a TV ad once or twice, therefore in most cases, reach should be prioritised.

In Depth

Background

The world of response has changed beyond all recognition. Gone are the days of dedicated phone numbers and plans based around the opening hours of call centres. Today we have a variety of devices at our fingertips and can respond to ads as and when we want; be it in store, on the phone, or more commonly, online.

As convenient as this may be for consumers, it’s muddied the waters for industry practitioners. Understanding how each medium co-exists and operates within the connected response environment is no mean feat. The flaws of last-click attribution are widely known, but we struggle to get a grip on how best to measure the impact of the different marketing channels when it comes to response, both in the short and long-term.

Thinkbox commissioned GroupM to examine the effects of different media channels in driving response, with a focus on understanding TV’s evolving, and often hidden, role.

GroupM analysed the impact of a range of channels, including brand response (BRTV) and direct response (DRTV) television, radio, print, outdoor, direct mail, affiliates, online display and paid online search on sales or orders via e-commerce, bricks and mortar outlets and the telephone. The study identified the additional levels of consumer response which was directly attributable to media investment over and above the ‘base’. The ‘base’ is the ongoing and underlying level of response which is the product of many factors, such as promotions, seasonality and the history of previous media investment.

GroupM employed a combination of analytics methodologies, including econometric modelling and their unique Spotlift tool, which analysed 1.38 million TV spots, spanning 43 advertisers and 9 sectors. Each methodology was tailored to the time period during which the effects of communications were measured: immediate (within 8 minutes), short to medium-term (0-3 months) and long-term (c. 3-24 months).

The analysis revealed the complexities of the integrated response system but also the wide ranging impact that television has across every element.

Findings

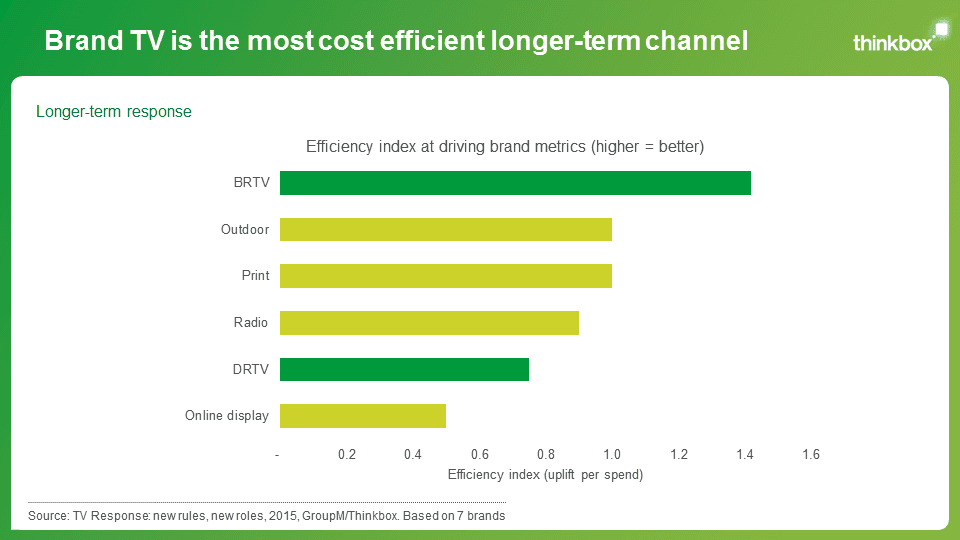

TV advertising dominates longer-term response

We know that communications work in the longer-term by driving consideration amongst those that might not currently be in the market for our brand. By investing in our brand we build our base of sales, which in turn makes our tactical communications more effective. By measuring just the short-term impact of our marketing communications, we miss out a vital part of the picture.

The study found that around half of all media-driven response comes in the long-term – that is within 3-24 months post-campaign. The longer-term impact of communications tended to be significantly larger for the kind of products which stimulate desire (such as cars) over those that we need (such as car insurance).

The analysis also revealed the impact of brand response TV (BRTV) and demonstrated that it was the most efficient driver of long-term response overall. BRTV was responsible for 52% of the long-term media impact. This backs up findings from previous studies, including the IPA’s ‘Advertising Effectiveness: the long and short of it’ (2013) which found that TV advertising is vital for long-term brand health.

BRTV advertising was 40% more efficient at driving long-term response per pound than the next best forms of communication, which were outdoor and print. Online display was the least efficient generator of long-term response with TV 180% more efficient.

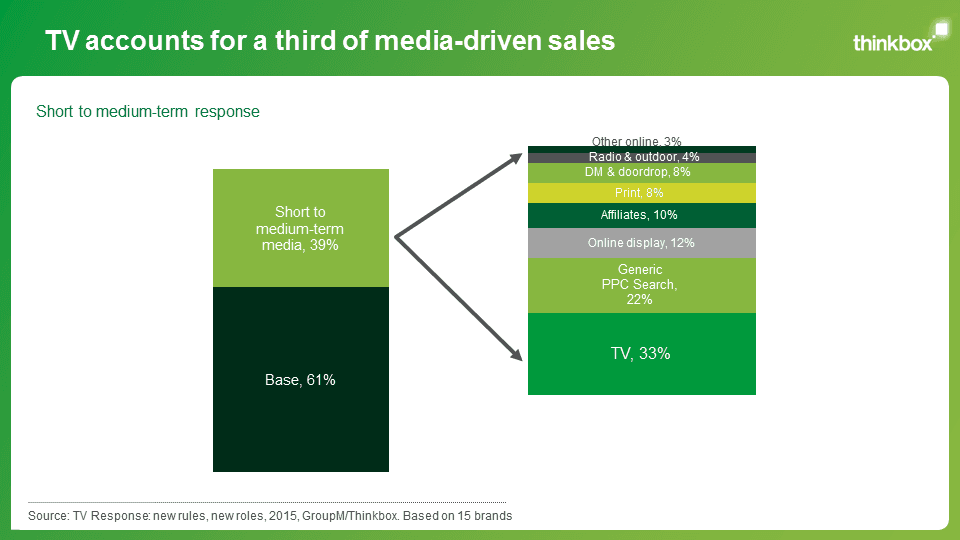

TV creates the most short to medium-term sales

The analysis showed that on average, media drove 39% of sales in the short to medium-term – i.e. within 3 months of a campaign finishing. The remaining 61% was comprised of the ‘base’ level of sales – which of course will have been significantly impacted by historical media activity, but also reflect elements such as seasonality, distribution or promotional activity.

TV advertising drove a third of these media-driven sales - more than any other communication channel. This was significantly higher than the next most impactful channel, which was generic pay-per-click search.

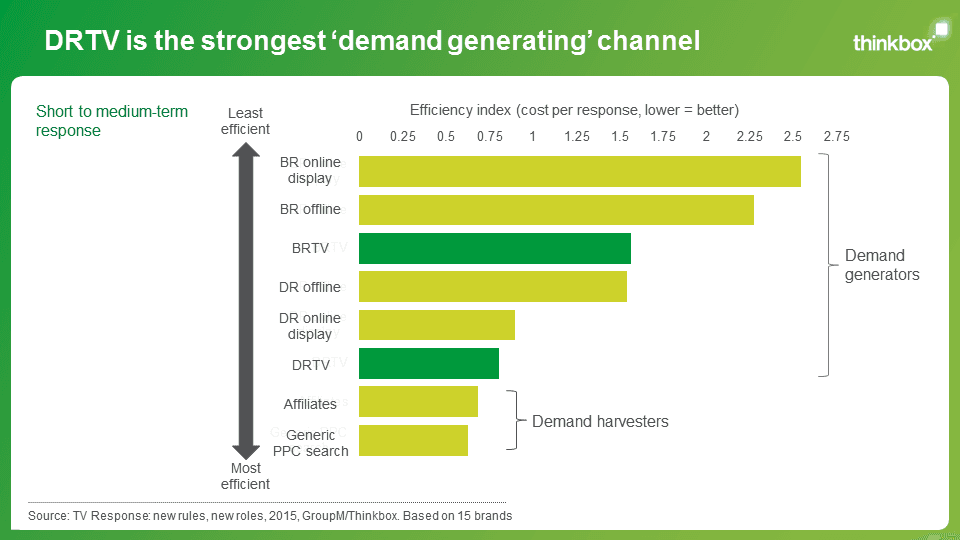

The work also demonstrated that DRTV was the strongest of the ‘demand generating’ channels – ie. the media types that are most likely to stimulate response rather than harvest it. DRTV was comparable in terms of efficiency with affiliate advertising and search marketing, even though the latter are demand harvesters rather than response generators.

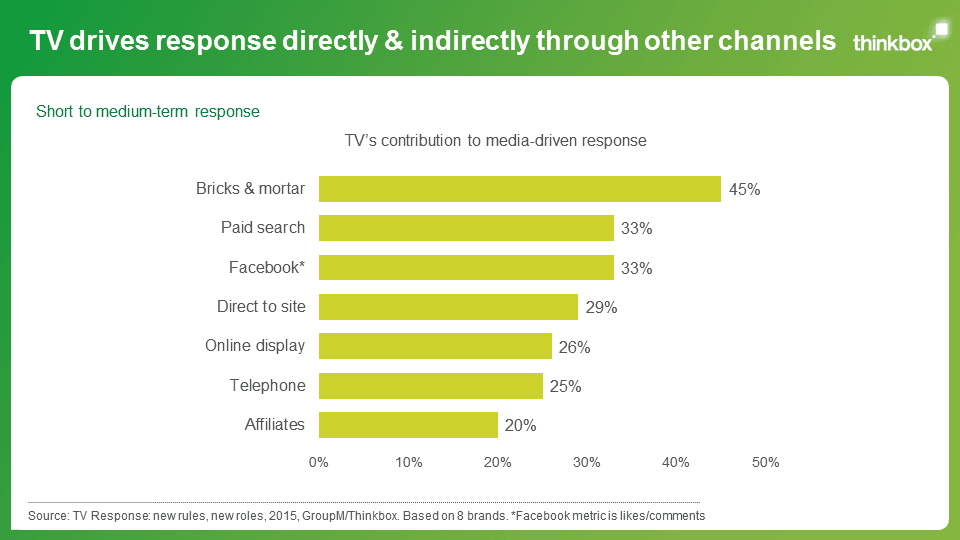

The study showed that TV has far reaching, but often hidden, effects across the entire communications system.

TV drove a response through several channels directly. It generated nearly a quarter (25%) of all media-driven sales delivered via the phone, 45% of all media-driven sales via bricks & mortar and 29% of media-driven sales through web traffic driven direct-to-site – this included natural search.

GroupM also discovered that TV drove an indirect response through online channels, generating 33% of media-driven sales via paid-for online search; 26% of media-driven sales via online display and a fifth of media-driven sales via affiliate marketing.

It also became apparent that TV had a significant impact on social media activity. TV was responsible for driving 33% of all media driven interactions for brands on Facebook. This could be likes or comments, for example. This effect of TV on social was two-fold. Firstly, we know that exposure to TV advertising prompts consumers to directly engage with social media. This has become increasingly apparent over recent years where ads such as the John Lewis Christmas TV ad cause a flurry of social media activity within moments of airing.

Secondly, as highlighted above, TV drives significant volumes of sales and many customers will be tempted to engage with social media after purchase to talk about their brand experience.

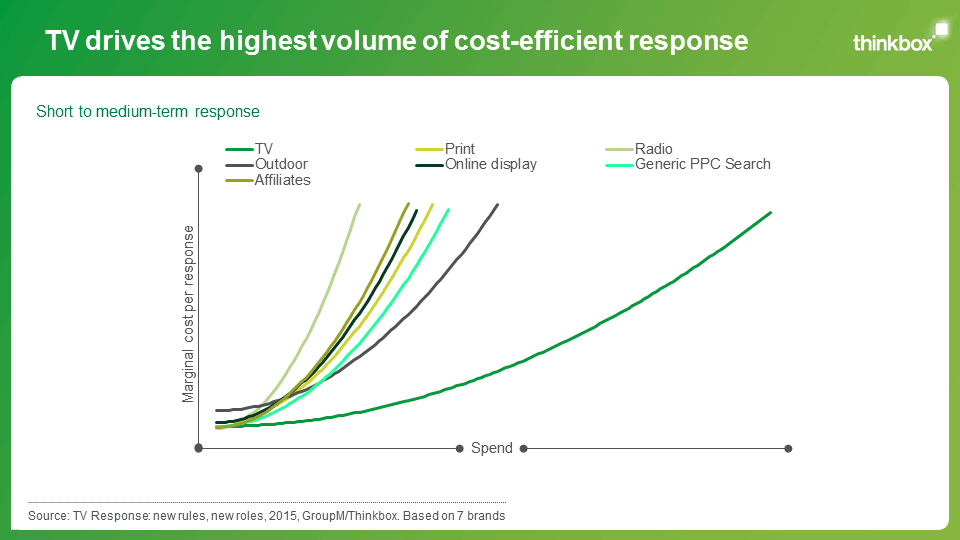

TV advertising drives the highest volume of cost-efficient response

One of the benefits of TV advertising is its ability to reach vast numbers of people and to reach them quickly. Because of its reach and scale, TV advertising keeps generating a cost-efficient level of response at higher levels of spend than other media.

Over the short to medium-term the point of diminishing returns is much lower for TV than it is for other media. To put it simply, the point at which the efficiency of ad spend starts to decrease significantly (because you have reached saturation and/or are repeatedly talking to the same people) - is much lower for TV than for the other communication channels.

This means there is more headroom to spend efficiently on TV than with any other media. This enables brands to drive a high volume of response and profit.

In fact, spend on TV advertising can be 2.7 times higher than online channels before there is a significant decrease in efficiency. It can be 2.5 times higher than print and 2.8 times higher than radio.

Direct response TV should be planned to maximise coverage above frequency

Modelling the level of response delivered per exposure for 6 direct response-focussed advertisers, GroupM found that approximately 90% of total response was generated after a viewer had seen an ad for the first or second time.

This turns conventional response planning wisdom on its head as the majority of direct response TV airtime is conventionally bought in daytime and optimised for frequency rather than reach.

Instead, direct response campaigns should maximise reach and minimise the number of times viewers are exposed to an ad more than twice.

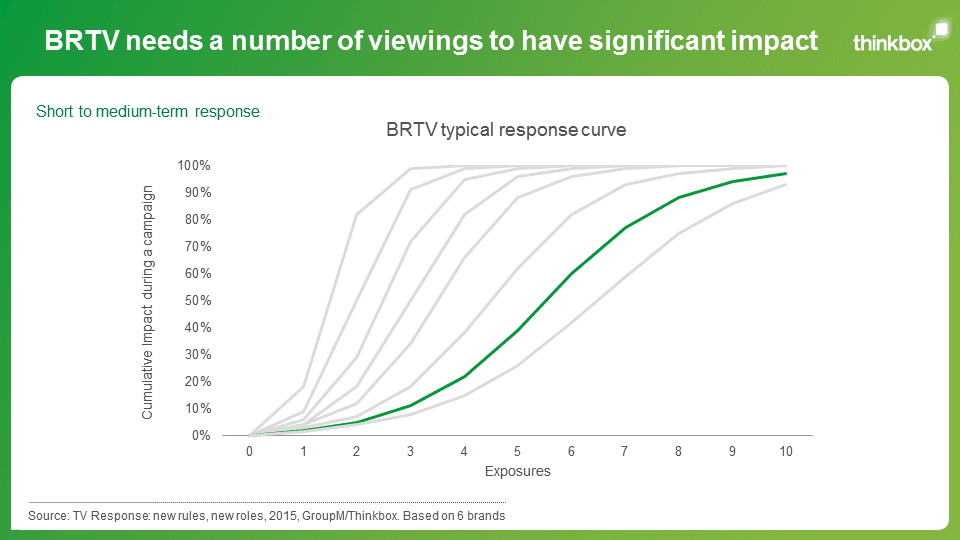

The reverse is true for BRTV airtime, where a number of viewings are needed in order for the impact to be felt.

Strategies to optimise the chance of immediate response

By analysing the data from their unique Spotlift tool, GroupM were able to measure the incremental uplift in response within 8 minutes of a TV ad airing. This involved the systematic examination of 1.38 million spots spanning 43 advertisers and 9 sectors. Several considerations became apparent when planning for immediate response.

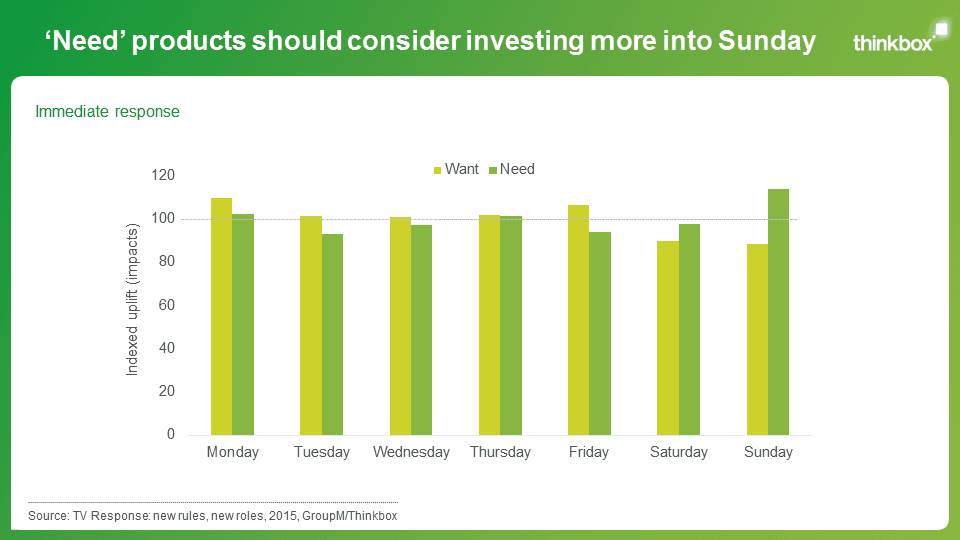

a) There is a clear difference between response to products that people need versus those that they want.

Responding to products that interest us, such as holidays or cars, is viewed as less of a chore. Subsequently, the times when we’re most likely to respond to these kinds of ad are inherently connected to our mood and frame of mind. We might be happy to while away an hour researching our next holiday on a Monday evening after work, but we probably wouldn’t do the same for our car insurance. Likewise, when Sunday rolls round, we’re often in more of a ‘doing mood’ – determined to get things done before the week ends.

It therefore makes sense to upweight ‘want’ brands earlier in the week (and on Fridays when we’re in a relaxed mood) over the products that we need – and vice versa.

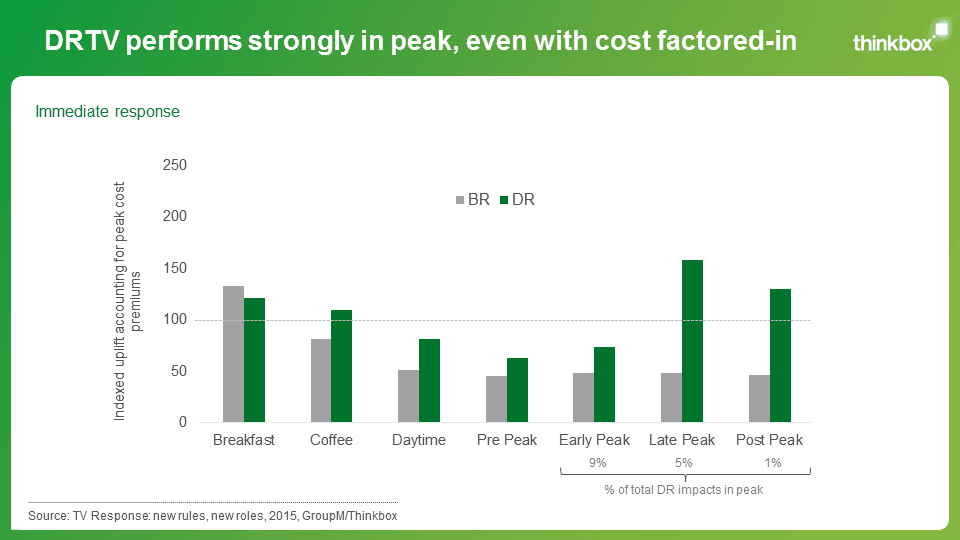

b) Peak is a strong performer

Whilst we tend to associate DRTV with daytime, the research shows that peak is a particularly strong time for response. The rise in multi-screening means that people now regularly watch TV with an accompanying device, meaning the opportunity for response is just a click or tap away. Of course, peak airtime costs more than daytime, but even when the cost of the airtime is taken into account, late-peak airtime still offers a significant opportunity for response.

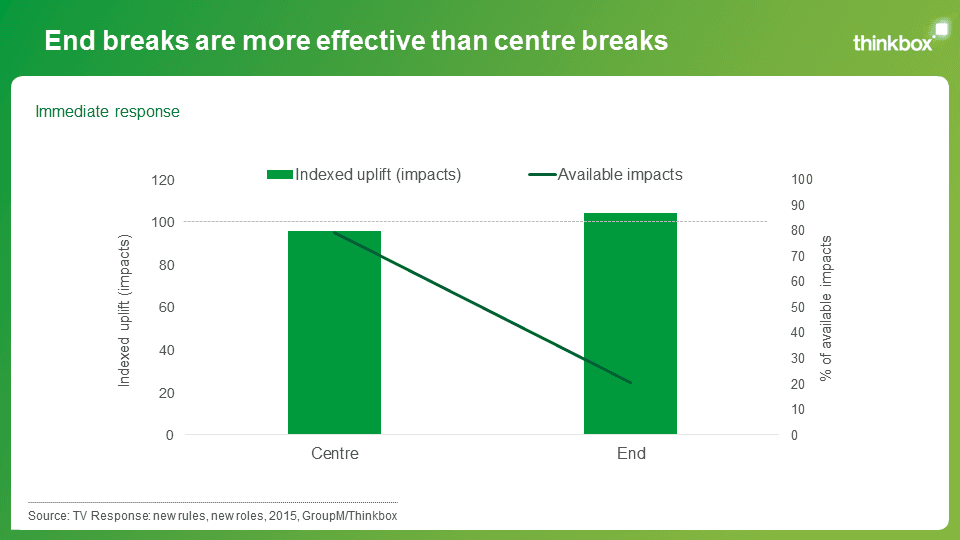

c) End breaks are more effective that centre breaks

Perhaps unsurprisingly, when it comes to response, end breaks are more efficient. Again, this is likely to be driven by behaviour, with viewers waiting until their programme has come to an end before heading off on an online journey.

d) Smaller spots tend to elicit the most immediate response.

Lower rating spots tend to be the most effective at driving an immediate response. This is likely to be driven by levels of engagement, with viewers less willing to compromise the viewing experience of a programme they are immersed in to go online.

However, although these spots are the most impactful when it comes to immediate response, they cannot drive scale and the research demonstrated that in most instances, coverage of DR campaigns should be maximised over frequency.

In summary

Although the world of response is undeniably complex, we finally have the tools to unlock the value of each media and understand where they sit within the integrated response system. We now know that TV has the most wide-ranging response effect and we can start to employ strategies that maximise the impact of our TV spend when it comes to driving response in both the short and long-term.